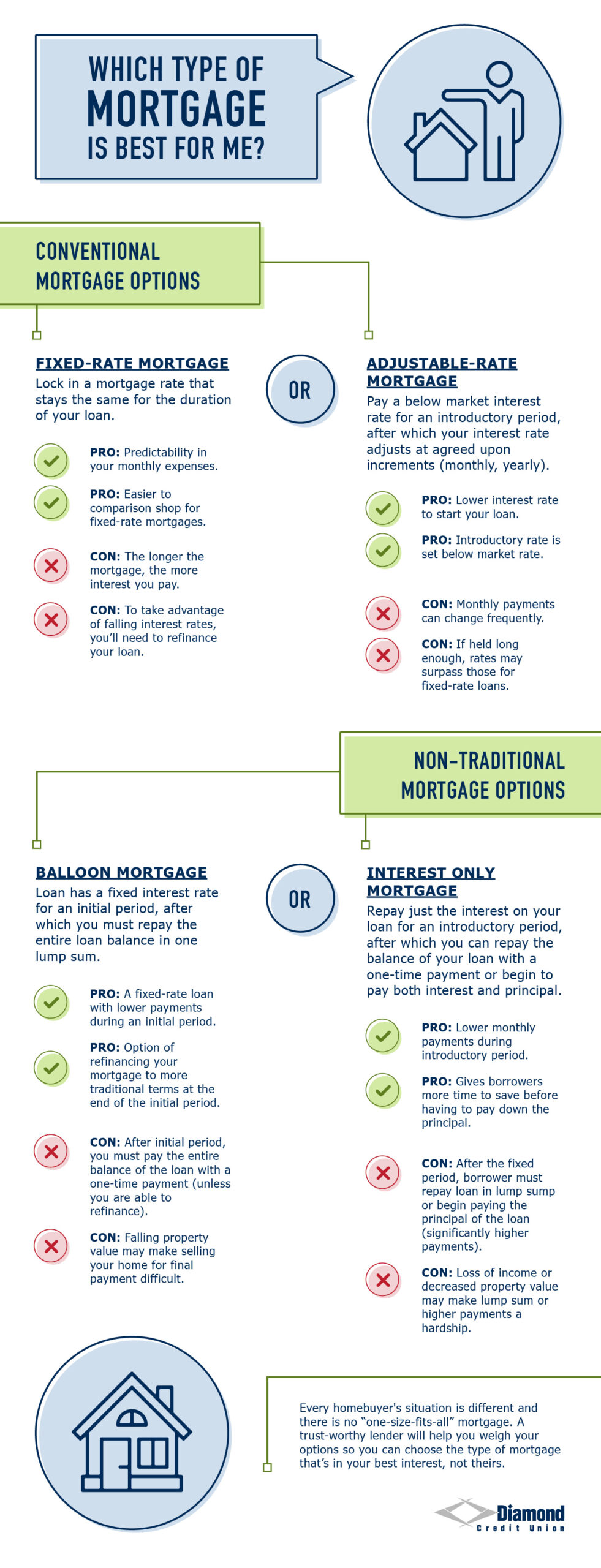

Which Types of Mortgage Loans are the Best?

There are quite a few different types of mortgage loans for you to choose from and knowing which one is best for your situation can be overwhelming.

{kind=link}

This guide will provide insight into the options available to you and information so you can make the smartest decision for you.

If you’re ready to talk through your mortgage options, Diamond’s mortgage experts are ready to help.

#1. Conventional Mortgages

This type of mortgage loan is made through a private lender and typically requires a higher credit score to qualify.

These loans are available through banks, credit unions, and mortgage companies. Later in this blog, we’ll discuss other home loan types offered through government entities like the Federal Housing Administration.

There are two different types of conventional loans, fixed-rate and adjustable-rate. Let’s compare the two.

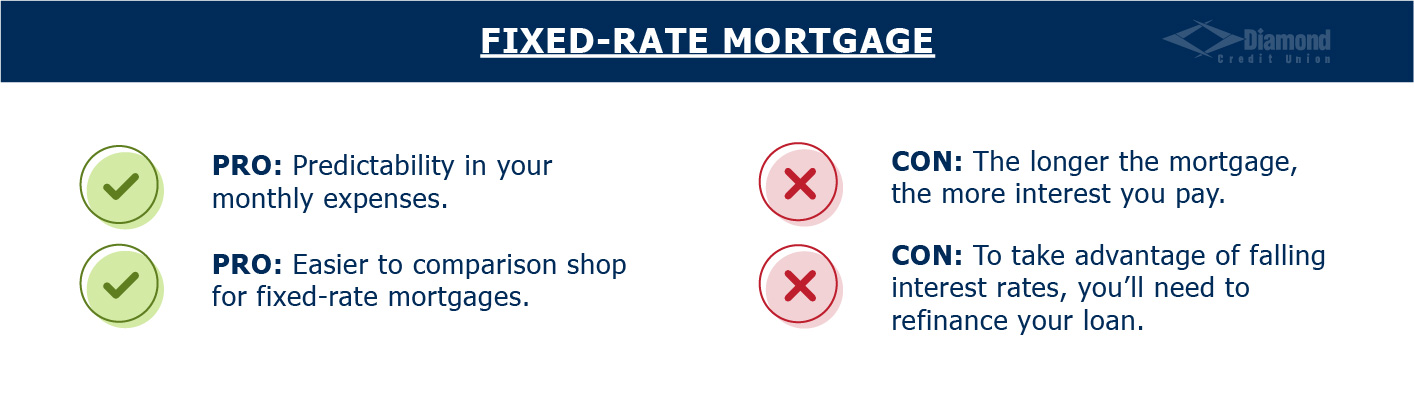

Fixed-Rate Mortgage

As the name suggests, a fixed-rate mortgage has the same interest rate for the duration of your loan. This provides you with a layer of predictability so you can better plan your monthly expenses.

You’ll notice the balance of principal and interest change, but your total monthly payment is the same. Because of this, you can easily compare fixed-rate mortgages across different companies or vendors by using a mortgage calculator.

There are a few downsides to fixed mortgages.

- If interest rates drop, you’ll need to refinance your loan to take advantage of this.

- The longer the mortgage, the more interest you will pay.

- To qualify, you need a good or excellent credit score.

Pros and Cons of a Fixed-Rate Mortgage

{kind=link}

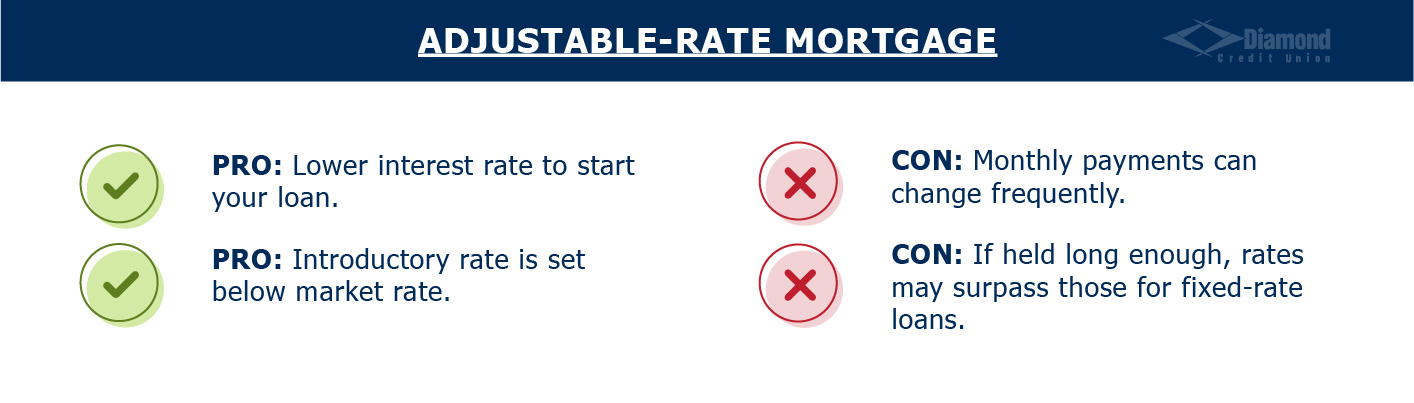

Adjustable-Rate Mortgage

On the other hand, an adjustable-rate mortgage will have an interest rate that fluctuates over time. An initial interest rate, typically set below market rate, is charged for a period of time depending on the lender.

After this specified time is completed, the rate adjusts incrementally for the remainder of the loan.

The benefit of an adjustable-rate mortgage is that you will likely start with a lower interest rate. As the borrower, you’ll also be able to qualify for a larger loan compared to a fixed-rate mortgage.

Similar to fixed-rate mortgages, there are some cons.

- Your interest will increase after the specific initial period and could potentially rise above what the fixed rate would be.

- Your monthly payments will change so there’s less stability for you to be able to plan your budget.

- Since this is a conventional mortgage type, you will need a good or excellent credit score to qualify.

Pros and Cons of an Adjustable-Rate Mortgage

{kind=link}

15-Year versus a 30-Year Conventional Mortgage

Just like there’s no right answer for choosing the best mortgage rate, there isn’t a clear path on whether you should choose a 15-year or a 30-year conventional mortgage.

A good rule of thumb is a longer plan will offer a lower monthly payment but a higher overall cost because of interest. A shorter plan will be a higher monthly payment but you’ll be paying less in interest costs.

There are other options to choose from when it comes to the term length of your loan. So to get a full picture of your options, speak with your lender to find the best scenario for your financial situation.

Diamond offers both types of conventional mortgages with the option for a 10, 15, 20, or 30-year loan type.

#2. Non-Conventional Mortgage Options

Although you may be immediately attracted to non-conventional loans because they allow borrowers to qualify for larger amounts, they are the riskier option overall.

These types of mortgage loans were created during the real estate boom in the early 2000s, with the idea that you’d be making more money or being able to become profitable from the sale of your house and be able to pay a higher monthly rate.

Unfortunately, as you probably already know, the housing market crashed and many borrowers then found themselves with mortgages they could no longer afford to repay.

There are still advantages to different non-conventional mortgage types, so let’s discuss these options further.

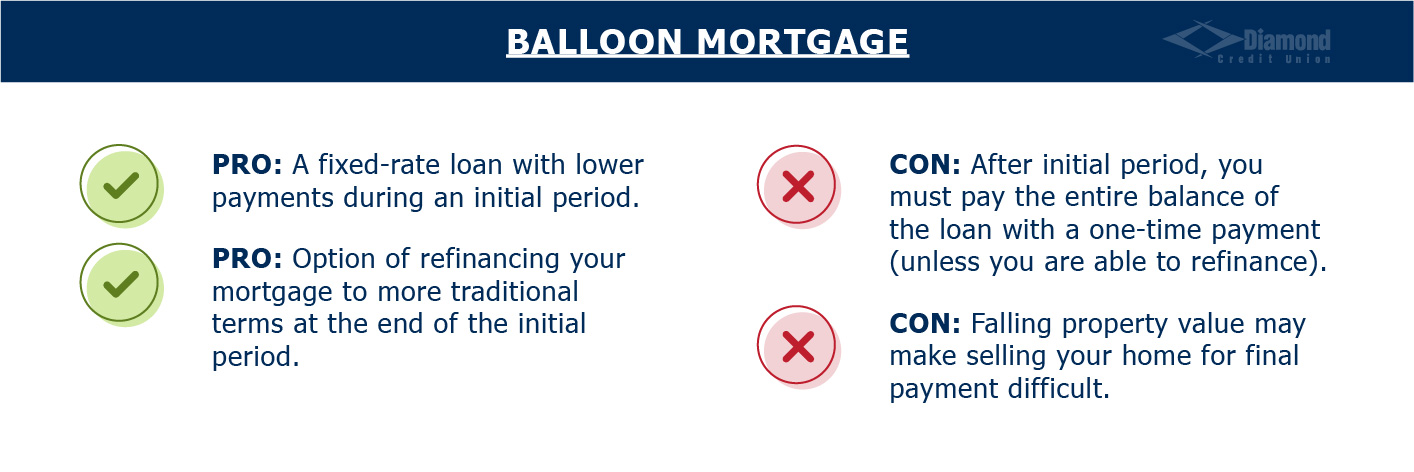

Balloon Mortgage

Balloon mortgages are certainly not as common as when they were first introduced into the housing market, however, they are still a viable option for you. This mortgage loan charges a lump sum payment at the end of your term.

So, let’s say your loan is for 5 years, you’ll start paying this loan right away. The difference is that the monthly payments are typically at a lower interest rate. After the 5 years or the length of your loan is over, you’ll be expected to pay the entirety of what’s left.

Typically, a loan is amortized so the monthly payments cover interest, principal, and other expenses. When the term is finished, you owe nothing. A balloon mortgage does not amortize your loan, so while the payments are lower, you have to be wary of when the loan ends and how much is left to repay.

An advantage to balloon mortgages is that at the end of your loan period, you may have the option to refinance to a more traditional loan. This would mean you’d continue monthly payments and would not need to pay the full amount right away.

Pros and Cons of a Balloon Mortgage

{kind=link}

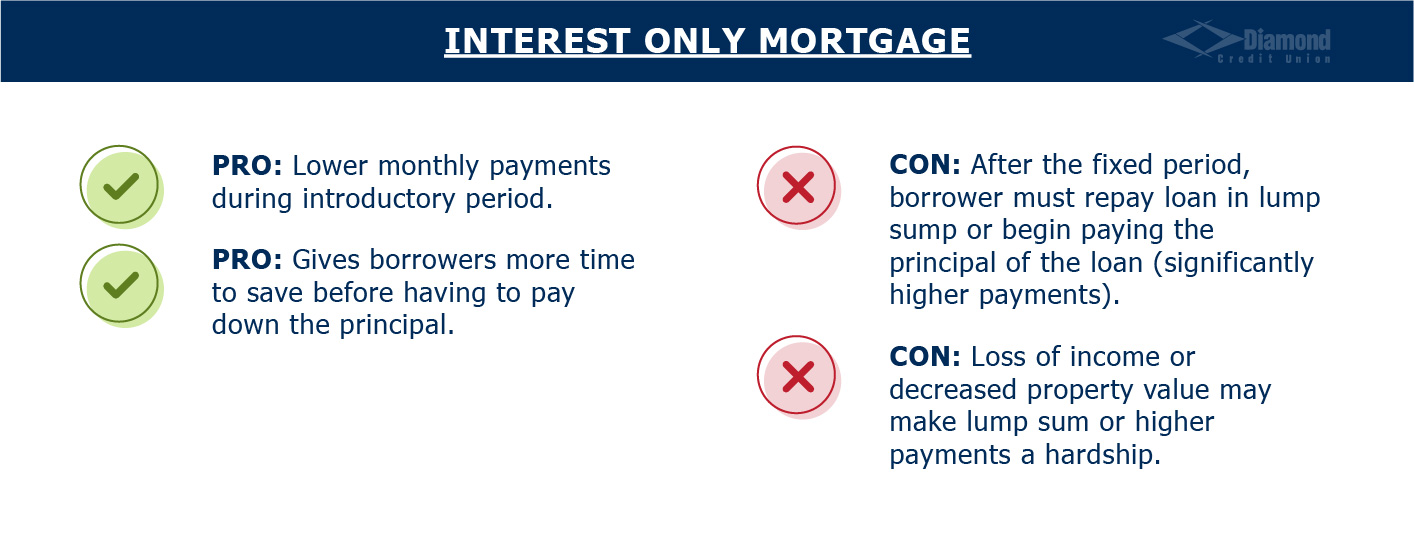

Interest-Only Mortgage

As the name suggests, an interest-only mortgage means you’re only paying the interest rate for a set time frame. Just like a balloon mortgage, when that initial period is over, you are expected to pay the lump sum of your loan or start paying both the interest and the principal.

Whether you’re paying the entirety of the loan or starting a monthly schedule, the payment will be significantly greater than when you were just paying interest. Sometimes it is doubled or even tripled than your initial payments.

And depending on whether or not your property value increases or decreases, you’ll face hardships when you need to pay higher payments.

Pros and Cons of an Interest-Only Mortgage

{kind=link}

#3. Government Issued Loans

The types of mortgage loans listed above are all ones that are given out by private lenders. Now, we are going to highlight some government-issued loans available for a variety of different demographics.

An overarching downside to these loans is that they all have specific requirements to qualify for the loan. Some examples include being a first-time homebuyer, having a specific income, or being a part of the military.

Federal Housing Administration (FHA) Loans

The Federal Housing Administration, also known as FHA, helps insure your loan so a lender can offer you a better deal. They also have a great index of resources that can connect you to homebuying programs in your state.

Reverse Mortgage Loans

The final type of mortgage loan is a reverse mortgage. This mortgage rate is only available to people who are 62 years or older. Essentially, this type of mortgage loan uses your existing home equity as a loan. Because of this structure, your home equity will decrease the more you use your reverse mortgage loan.

Because you are using your home equity, even if you move out of the home, you are still required to pay the loan. Just like the other home loan types, interest and fees will accumulate over time.